SME Debtors’ Equity Retention: Comparing the Relative Priority Rule with the Fair and Equitable Test

1. Introduction

SME Debtors are the backbone of the economy in both the European Union (EU) and

the United States of America (US)[1] and yet, they are the ones which run the risk of being liquidated.[2] The COVID-19 pandemic has only exacerbated this problem.[3] It is therefore important to have a restructuring process which enables the SME Debtors in financial difficulties to continue business while balancing the rights of all parties involved.[4] For successfully reviving SME Debtors through restructuring, equity retention may be crucial. SME Debtors are often heavily dependent on the entrepreneur’s managerial skills, connections and expertise for their business.[5] At the same time, the goal of a successful restructuring is to not only retain equity but also balance the rights of creditors and other stakeholders.[6] There is a conflict related to the nature of entitlement of debt claims distribution amongst the creditors and equity holders during restructuring referred to as the debt/equity bargain (‘Debt/Equity Bargain’).[7] A plan for restructuring a debtor may be adopted by the affected parties[8] by voting or confirmation by the court.[9] Certain restructuring plans which affect the claims or interests of dissenting affected parties shall only be binding if they are confirmed by way of a cram-down by the court.[10]

EU Directive 2019/1023 on preventive restructuring framework (Directive 2019/1023) strives to balance the Debt/Equity Bargain by including two alternative Fairness Tests of priority, (i) the Absolute Priority Rule[11] and (ii) the Relative Priority Rule.[12] These fairness tests have to be fulfilled to satisfy the cram-down requirement. The last-minute inclusion[13] of the Relative Priority Test under the Directive 2019/1023 triggered a heated scholarly debate[14] on whether the Absolute Priority Test should be preferred instead of the Relative Priority Test. Interestingly, it has been suggested by legal scholars that although Directive 2019/1023 incorporates the Relative Priority Test based on its theorisation by legal scholars in the US, the Relative Priority Test has not been incorporated in the same form as theorised in the US.[15] However, in the US, the Small Business Reorganization Act of 2019 was introduced to streamline the restructuring of SME Debtors.[16] Instead of incorporating the Relative Priority Test, a new Fairness Test – the Fair and Equitable Test - was introduced under the Small Business Reorganization Act of 2019. This Fair and Equitable Test mandates that SME Debtors repay creditors while retaining equity in the form of Projected Disposable Income.[17]

This paper analyses the extent to which the Relative Priority Test enables equity retention for SME Debtors, by comparing it with the Fair and Equitable Test under the Small Business Reorganization Act of 2019. I will compare Article 11(1)(c) of Directive 2019/1023 which provides the Relative Priority Test with Section 1191(c) of the Small Business Reorganization Act of 2019, which prescribes the Fair and Equitable Test. For this purpose, I conduct a literature review and quantitative analysis based on equity retention indicators for SME Debtors. In Section 2, I will introduce the basic concepts such as the Debt-Equity Bargain, the Best Interest of Creditors Test and Fairness Tests which will enable us to review the importance of equity interest retention for SME Debtors during restructuring. In Sections 3 and 4, I will outline how the Relative Priority Test under Directive 2019/1023 and the Fair and Equitable Test under the Small Business Reorganization Act of 2019, enable equity interest retention for SME Debtors. Thereafter, in Section 5, I compare the Relative Priority Test with the Fair and Equitable Test through quantitative analysis and use the results to compare how this can impact equity retention indicators. I will finally conclude this paper by providing suggestions for the implementation of the Relative Priority Test in a manner that facilitates equity retention interests for SME Debtors, by finding orientation under the Fair and Equitable Test.

2. Importance of Equity Retention for SME Debtors during their restructuring

Equity retention for SME Debtors is crucial for their revival since the viability of an SME Debtor may depend on the same person(s) combining the role of manager and residual risk-bearer (i.e. the equity holder).[18] The SME Debtor may strongly rely on the equity holder’s cum manager’s connections, skills and regional expertise to successfully revive, upon its restructuring.[19] Equity retention incentivises equity holding management to access a restructuring process at an early stage to prevent the liquidation of the SME Debtor. This is particularly important because a delay in accessing restructuring could result in a worse outcome for the creditors.[20] Shareholders may also be interested in early restructuring because their equity shares are affected and devalued before the creditors’ claims.[21]

Having highlighted the necessity of equity retention for SME Debtors, I will now briefly review the peculiar characteristics of SME Debtors. Based on this review, I arrive at a working definition of the SME Debtors (‘Working Definition’), which is used as a practical point of reference, for conducting the comparative analysis in this paper.

2.1 Working Definition of SME Debtors

An SME Debtor has been defined differently in the domestic laws of different EU Member States and the US.[22] The Directive 2019/1023 states that the concept of SME is to be understood by reference to the national law of Member States.[23] The definition under Directive 2019/1023 is therefore rather broad. It includes a wide range of enterprises from the sole entrepreneur or artisan to a company of 250 employees with a turnover of EUR 50 million annual turnovers.[24] However, the Small Business Reorganization Act of 2019, does not provide a definition for SMEs based on the number of employees or turnover. It stipulates that a debtor is eligible to apply for restructuring proceedings under the Small Business Reorganization Act of 2019, if the debtor is engaged in commercial or business activities that does not exceed the financial debt thresholds of aggregate debts stipulated under the law.[25] Evidently, there is no uniform definition of SMEs.

Given this inconsistency, I follow a functional approach similar to the one adopted in the Report of the European Law Institute on Rescue of Business in Insolvency Law (‘ELI Business Rescue Report’).[26] Instead of focusing on the qualification thresholds, I look at the peculiar SME Debtor characteristics which necessitate equity interests’ retention in them during a restructuring. Literature suggests that these characteristics of an SME Debtor include:

- Limited resources and lack of access to finance,[27]

- Interdependency with entrepreneurship, having closely intermingled business and personal debts,[28]

- Suffering from creditor passivity,[29]

- Lack of incentives to access restructuring at an early stage of the formal insolvency process[30] and

- From a macroeconomic perspective, the failure of a business might also lead to failures in the supply chain since its customers are also SMEs and depend heavily on timely payment.[31]

This Working Definition of SME Debtors has been used to conduct the comparative analysis for testing the Relative Priority Test and the Fair and Equitable Test, in the subsequent sections.

2.2 Challenges with equity retention - The Debt-Equity Bargain

The goal of the restructuring process, both under the Directive 2019/1023 and the Small Business Reorganization Act of 2019, is to enable an SME Debtor in financial difficulties to continue its business while balancing the rights of all parties involved, including the creditors.[32] A debtor’s restructuring plan may be adopted by the affected parties[33] by voting or by confirming a plan by the court.[34] There is, however, a fundamental conflict related to the manner and quantum of entitlement of claims amongst the creditors and equity holders during restructuring. This is called the Debt/Equity Bargain.[35]

The concept of the Debt/Equity Bargain is based on the idea that a creditor’s legal rights are forcibly rewritten in a way that is detrimental to them, at least, prima facie. Therefore, equity interests’ retention at the cost of creditor’s interests might be unjustified.[36] This Debt/Equity Bargain is fundamental to the discussion of whether equity interests should be retained during restructuring. Creditors are in principle entitled to be paid before equity receives anything. However, they cannot gain any additional benefits. They may claim only against the debtor’s assets and have no recourse to its equity holders. Equity holders are residual claimants and not entitled to any particular return at all, any such return being contingent on the prior satisfaction of the debt claims.[37] This implication of the Debt/Equity Bargain has often been debated due to the risk of its abuse by creditors.[38] It has been suggested by scholars that the process of preventive restructuring should be differentiated from other modes of insolvency where the revival of business may not be the priority.[39] As stated earlier, in the case of restructuring of SME Debtors, retention of equity interests’ may be crucial for the successful restructuring of the business. Therefore, the question of whether creditor interests should always and fully trump the interest of equity holders has been much debated.[40]

To govern this Debt-Equity Bargain, while confirming restructuring plans, the court is required to ensure that the plan satisfies the Best Interest of Creditors Test and in cases of dissenting affected parties, additionally the Fairness Tests.[41]

2.3 Application of Best Interest of Creditors Test and Fairness Tests

The Best Interest of Creditors Test requires that no dissenting creditor is worse off under a restructuring plan than it would be in the case of liquidation.[42] Directive 2019/1023 additionally stipulates the satisfaction next-best alternative scenario instead of liquidation, as a baseline requirement for testing whether the creditors are in a worse-off position.[43] The next-best-alternative scenario has been interpreted by academicians to be a scenario which is realistically likely to materialise if the plan were not approved.[44] It aims to guarantee the realisable value of existing claims and equity rights of dissenting stakeholders (‘Realisable Value’). The surplus generated under a restructuring plan, based on the cooperation of stakeholders as a going concern by providing, for instance, future finance, workforce and supplies, may be referred to as the ‘Reorganisation Surplus’.[45] The Best Interest of Creditors Test sets a baseline for a minimum distribution of the realisable value. The Fairness Tests of the Absolute Priority Test, Relative Priority Test and the Fair and Equitable Test set the baseline for determining the fairness of the distribution of the expected Reorganisation Surplus to be achieved under the restructuring plan which is required to be confirmed.[46] I will scrutinise and compare two Fairness Tests, the Relative Priority Test and the Fair and Equitable Test in further detail in the subsequent sections and outline how they enable equity interests’ retention for SME debtors during their restructuring.

3. Equity Interests’ Retention under the Relative Priority Test

In the previous section, I laid the foundation by discussing why equity retention is important for SME Debtors and the role played by Fairness Tests in enabling such equity retention in SME Debtors during their restructuring. In this section, I will discuss the cross-class cram-down conditions for the application of the Relative Priority Test under Directive 2019/1023 and how it enables equity interests’ retention for SME Debtors during their restructuring.

3.1 Cross-class cram down under Directive 2019/1023 for the application of Relative Priority Test

Under the Directive 2019/1023, the Relative Priority Test as a fairness test is applied only in situations of cross-class cram-downs. Any restructuring plan that (i) affects the claims or interests of dissenting affected parties, or (ii) provides for new financing, shall be binding only if the plan is confirmed by a court by a cross-class cram-down.[47] A cross-class cram down is operational if the majority percentage for affected parties in every voting class has not been achieved. The restructuring plan will become binding on these dissenting voting classes only if it is approved by the court by way of a cram-down.[48] For a cram-down to be applicable, firstly, a restructuring plan should satisfy the Best Interest of Creditors Test. It should treat the creditors with a sufficient commonality of interest in the same class and in a manner proportionate to their claim. Additionally, it should have a reasonable prospect of preventing the insolvency of the debtor or ensuring the viability of the debtor’s business.[49] It has to be approved by a majority of the voting classes of affected parties, provided that at least one of those classes is a secured class of creditors or is senior to the ordinary unsecured creditors class; or at least one of the voting classes of affected parties, other than equity-holders class, or any other class, which upon a valuation would not receive any payment.[50] No class of affected parties should receive or keep more than the full amount of their claims.[51]

Once the above-mentioned conditions have been satisfied, the Directive 2019/1023 provides for the Relative Priority Test and the Absolute Priority Test as Fairness Tests, which are to be satisfied for the operation of a cross-class cram-down.[52]

3.2 Relative Priority Rule and its Relaxed Approach under the Directive 2019/1023

Article 11(1)(c) Directive 2019/1023 incorporates the Relative Priority Test under the Directive 2019/1023. The Relative Priority Test requires that dissenting voting classes of affected creditors are treated at least as favourably as any other class of the same rank and more favourably than any junior class.[53] It has however been suggested by scholars that the Directive 2019/1023 fails to clarify the standard for treating a senior class ‘more favourably’ than a junior class’.[54] Although these arguments might hold ground, it is assumed for the purposes of this Paper that senior creditor classes would be treated ‘more favourably’ if they receive a greater percentage distribution on their claims than any other junior class.[55]

In certain situations, equity holders may be required to be paid in full, while the creditors may not be paid in such a manner. However, such a distribution mechanism cannot be confirmed under the Relative Priority Test, when applied in its strictest sense, since the creditors are required to be provided with a relatively better treatment before providing value to the equity holders.[56] In such a situation, the Directive 2019/1023 provides for a general derogation from the priority rule under the second paragraph to Article 11(2) to allow for the so-termed ‘Relaxed Relative Priority Test’.[57] The derogations from Article 11(1)(c) are only permissible if:

- It is necessary in order to achieve the aims of the restructuring plan; and

- the restructuring plan does not unfairly prejudice the rights or interests of any affected parties.[58]

This Relaxed Relative Priority Test approach has been suggested to be justified in governing the Fairness Test in cramdown situations.[59] It is pertinent to note that SME Debtors may be exempted by Member States from (i) the obligation to treat affected parties in separate classes and (ii) satisfy the requirements of a cross-class cram down mechanism and resultantly, the Fairness Tests of the Relative Priority Test and the Absolute Priority Test.[60] In the event these exemptions are provided, then the Fairness Test of the Relative Priority Test would not be applicable in the first place. For practical purposes, this paper assumes that SME Debtors have not been exempted from these requirements.

3.3 Enabling Equity Interests’ Retention for SME Debtors

Having looked at the manner in which the Relative Priority Test is applied, it is useful to look at its equity retention enabling ability. Subsequently, based upon this scrutiny, I shall be embarking upon a quantitative analysis to discuss the extent to which the Relative Priority Test enables equity retention in comparison to the Fair and Equitable Test.

The Relative Priority Test, in comparison to the Absolute Priority Test, increases the chances of awarding more value under the plan to equity holders.[61] In the event a Relaxed Relative Priority Test approach is adopted, it is possible for the equity holders to retain 100% of their pre-petition rights while refraining from making full payments to the creditors.[62] It has been suggested that the Relative Priority Test protects the relative position of dissenting classes of creditors without creating hold-out incentives.[63] The Relative Priority Test makes it more feasible for plans to be confirmed that permit equity holders to retain a stake in the debtor or its business. This may incentivise greater and more timely use of restructuring proceedings by SME Debtors.[64] Secured creditors may impose unreasonably onerous terms for providing credit by creating collateral on the SME Debtor’s assets. Such terms may be imposed with the intention of obtaining equity interests in exchange in the event of restructuring of an SME Debtor. The Relative Priority Test provides protection to equity holders from secured creditors who might impose unreasonably onerous terms for providing credit by creating collateral on the SME Debtor’s assets.[65]

At the same time, it has been suggested by scholars that the introduction of the Relative Priority Test may distort the insolvency process which transfers wealth from creditors to shareholders. It has been reasoned that Relative Priority Test may, thus, further undercut the position of SME Debtors.[66] It has been argued that equity holders may be able to opportunistically orchestrate the need for restructuring and retain value at the cost of creditors. Equity holders, thus, would no longer be dissuaded from taking excessive risks since they will no longer risk being wiped out first.[67]

In the next section, I will discuss how the Fair and Equitable Test enables equity retention for SME Debtors and thereafter, in the subsequent section compare the Relative Priority Test and the Fair and the Equitable Test.

4. Equity Interests’ Retention under the Fair and Equitable Test of the Small Business Reorganization Act of 2019

In this section, I will briefly outline the application of the Fair and Equitable Test of the Small Business Reorganization Act of 2019, and touch upon how it enables equity retention for SME Debtors during their restructuring.

Small Business Reorganization Act of 2019, was enacted to ‘streamline the bankruptcy process by which the small business debtors reorganise and rehabilitate their financial affairs’.[68] Under the Small Business Reorganization Act of 2019, only the debtor has an exclusive right to file a restructuring plan, in exclusion to all other parties.[69] A restructuring plan must be accepted by all affected classes to be confirmed.[70] In the event the plan is not confirmed consensually, it may be confirmed by way of a cram-down.[71]

4.1 Cram down of a restructuring plan under the Fair and Equitable Test

The court may cram down a plan even if no affected class of claims accepts the plan, as long as the plan does not discriminate unfairly and the Fair and Equitable Test requirement has been satisfied, with respect to each affected class of claims or interests that have not accepted the plan.[72] Pertinently, the Best Interest of Creditors Test is applicable during cram down and offers protection to the creditor who has not accepted the plan by mandating that the creditor must receive under the plan property with a value not less than what the creditor would receive if the debtor were liquidated.[73] Broadly, three sets of requirements for a cram down are to be satisfied (i) stipulations for secured creditors (ii) stipulations for unsecured creditors (in the form of the Projected Disposable Income) (iii) Remedies and requirements for feasibility.[74]

The plan may be crammed down notwithstanding the dissent of a secured creditor class if it permits the secured creditors to retain their lien on the property; the lien securing the allowed claim held by the secured holder.[75] Additionally, the plan must provide for secured creditors to receive on account of the allowed secured claims, payments, either present or deferred, of a principal face amount equal to the amount of the debt or collateral.[76] The secured creditors’ claim should also be satisfied by providing a lien on similar collateral. Cash payments less than the secured claim amount would not satisfy this requirement.[77]

The cram-down confirmation imposes a Projected Disposable Income test with respect to unsecured creditors.[78] The Projected Disposable Income of the debtor to be received in the 3-year period after the first payment under the plan is due, or in such a longer period not to exceed five years, should be applied to make payments towards the plan.[79] Alternatively, the plan may provide that the value of the property to be distributed under the plan within the 3-year or longer period is not less than the Projected Disposable Income of the debtor.[80] The Projected Disposable Income is the income that is received by the debtor and not reasonably necessary to be expended, either for the maintenance of the debtor or its dependent or for a domestic support obligation that first becomes payable after the date of filing of the petition.[81] It also excludes income necessary for the payment of expenditures necessary for the continuation, preservation or operation of the business.[82] The courts are given the discretion to decide the length of the commitment period.[83] A 3-year term is the baseline requirement.[84] For SME Debtors, this has usually been considered to be appropriate.[85]

The SME Debtor should be able to make all payments under the plan,[86] or the court must be able to assess that there exists a reasonable likelihood that the SME Debtor will be able to make all such payments.[87] The reasonable likelihood (‘Reasonable Likelihood Test’) requirement requires showing that the debtor can realistically carry out its plan. Though a guarantee of success is not required, the bankruptcy court should be satisfied that the reorganised debtor can stand on its own two feet.[88] The plan should also provide appropriate remedies including liquidation of non-exempt assets, to protect the holders of claims or interests in the event the payments are not made (‘Default Remedies Test’).[89] The Default Remedies Test does not require anything beyond the preservation of a creditor’s right to seek the enforcement of the plan terms in the bankruptcy court and seek appropriate relief from the court.[90]

4.2 Enabling Equity Interests’ Retention for SME Debtors

After two years of the enactment of the Small Business Reorganization Act of 2019, it has been suggested by scholars that it has been ‘monumental financially and psychologically’ for SME Debtors; making ‘equity holders, winners’ in restructuring by removing the Absolute Priority Test and thereby allowing the equity holders to retain their interests while coming up with a restructuring plan to make payments to the creditors within a period of three to five years.[91] Further, the requirement that the SME Debtor receives the acceptance of at least one impaired class has been eliminated. A restructuring plan may be confirmed even without the approval of any class of creditors.[92] An SME Debtor whose plan receives an immediate discharge instead of a discharge only at the end of plan payments encourages consensual confirmation of a plan, as opposed to a cram-down confirmation.[93] The Reasonable Likelihood Test and the Default Remedies Test protect the interests of creditors, who have the option of liquidating the SME Debtor’s assets upon the default of the restructuring plan.[94]

That having been said there could be issues for SME Debtors under the Fair and Equitable Test which may hinder equity interests’ retention during restructuring:

- The pre-petition equity holders might not be incentivised to stay and work for the SME Debtor since they would have to work, not to earn profits from the business but to pay the creditors for a period of three to five years.[95]

- In the event of the inability of the SME Debtor to come up with Projected Disposable Income that satisfies the Fair and Equitable Test, the plan may be rejected or the case may be converted into a Chapter 7 bankruptcy case where proceedings for winding up and bankruptcy of the SME Debtor may be initiated.[96] Therefore, the SME Debtor who is not in a condition to satisfy the test given the business conditions may risk having its assets liquidated.

- It has been argued that the Small Business Reorganization Act of 2019, does not provide many incentives for creditors to consent to a plan. Primarily, the unsecured creditors may see their interests being damaged under the Small Business Reorganization Act of 2019 since they are poorly positioned to defend against the erosion of their interests and usually have little financial incentives to do so.[97]

5. Comparing the Relative Priority Test with the Fair and Equitable Test

Having looked at the requirements for the application of the Relative Priority Test and the Fair and Equitable Test, in this section I will compare their equity interests’ retention ability by conducting a quantitative analysis and comparatively scrutinise them based on certain indicators.

The Relative Priority Test in Directive 2019/1023 under Article 11(1)(c) only mandates that dissenting voting classes are treated as favourably as any other class of the same rank and more favourably than any junior class. A Relaxed Relative Priority Test approach allows derogations from this rule if this is necessary to achieve the aims of restructuring and the plan does not unfairly prejudice the rights or interests of affected parties. Under the Small Business Reorganization Act of 2019, no priority tests (Absolute Priority Test or Relative Priority Test) are mandated. Instead, the satisfaction of the Fair and Equitable Test under 11 USC § 1191(c) is required. Broadly, it lays down 3 sets of requirements for a cram down (i) stipulations for secured creditors under sub-section 1191(c)(1), (ii) stipulations for unsecured creditors (in the form of the Projected Disposable Income) under sub-section 1191(c)(2) and (iii) Remedies and requirements for feasibility under sub-section 1191(c)(3).

The Directive 2019/1023 harmonises the restructuring laws while providing flexibility to Member States to apply their own procedural laws. Member States differ vastly on the order of priorities.[98] Certain Member States, for instance, France, Italy and Portugal, prioritise secured creditors.[99] Therefore, it could not have been possible to have separate priority rules for secured and unsecured creditors under Directive 2019/1023.[100] On the other hand, the Fair and Equitable Test has separate rules for priority, for each class of secured and unsecured creditors.[101]

5.1 Hypothetical Restructuring case to compare distributional possibilities

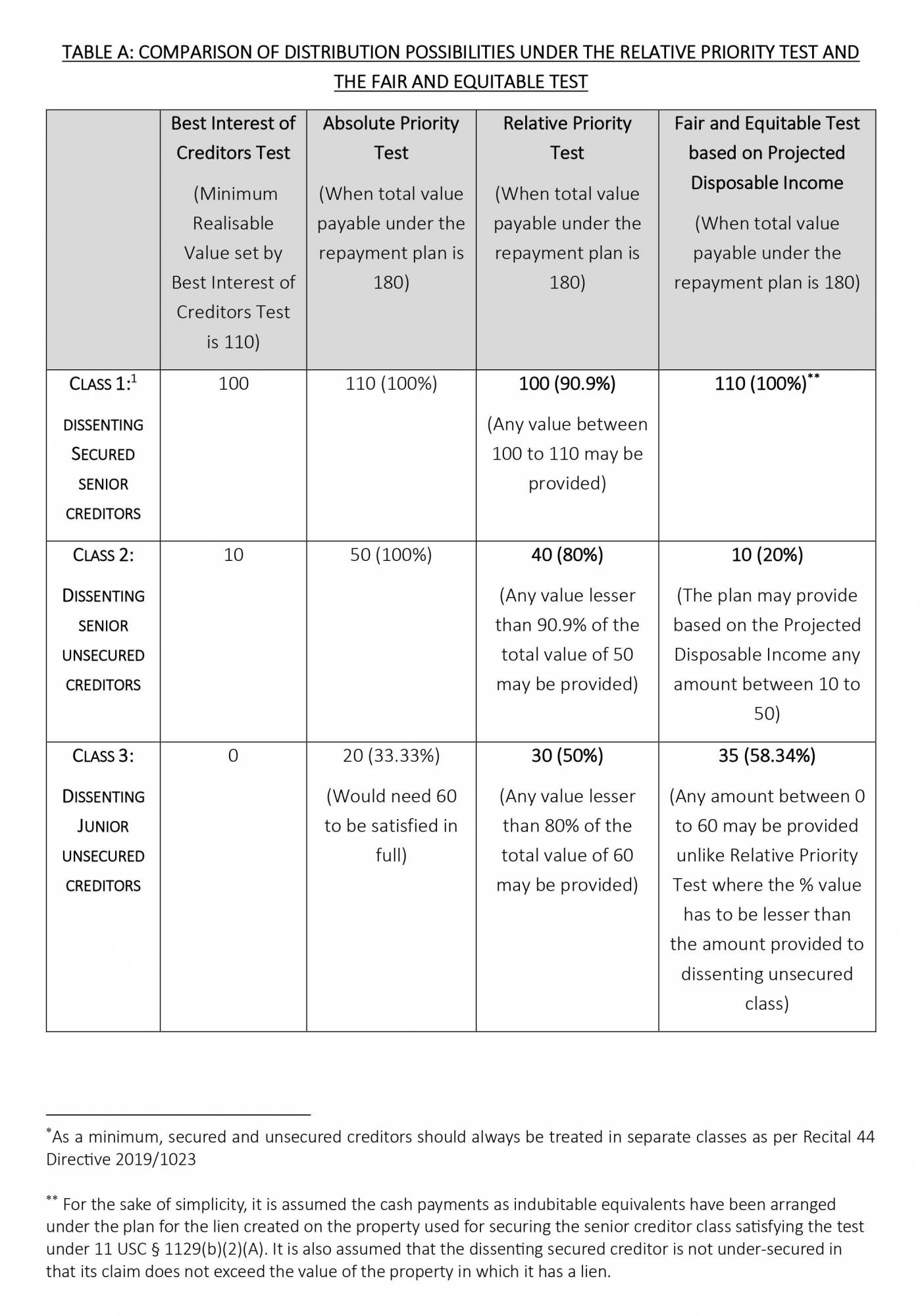

To compare how the Relative Priority Test and Fair and Equitable Test work out in a restructuring case involving an SME Debtor, I conduct a quantitative analysis in this section to analyse the distributional possibilities. In order to understand this comparison better, I take hypothetical figures, largely based on Madaus’ illustration.[102] I assume that if the Best Interest of Creditors Test is applied, a senior creditor class could expect 100, the unsecured creditors could expect 10 and the junior dissenting unsecured creditors and equity are not left with any value. The Reorganisation surplus is 70; therefore, the total value based on the restructuring plan is 180. For the full satisfaction of their value, the classes of creditors and equity holders need to be paid the following amounts, (i) secured creditors – 110, (ii) senior dissenting unsecured creditors – 50, (iii) Junior dissenting unsecured creditors – 60 and (iv) equity holders – 25 (Table A). I assume for practical convenience that the payment under the repayment plan has to be made within a 3-year time period since under both the Small Business Reorganization Act of 2019, and the Directive 2019/1023 a 3-year time period for making repayments under the restructuring plan is considered appropriate.[103] The class formation in this Table has been made in line with the requirements under Recital 44 and Article 9(4) Directive 2019/1023 which mandates that creditors of secured and unsecured claims are treated in separate classes. It is assumed that the claims and interests of every individual class are substantially similar. In line with the requirements under 11 USC §1191(b), the plan does not discriminate unfairly between different classes.

Data in this Table shows the following key features in the distributional possibilities under the Relative Priority Test and the Fair and Equitable Test:

i. Dissenting Secured Senior Creditors

Under the Relative Priority Test, the dissenting secured senior creditors class may receive any value between 100 to 110 i.e., 90.9% to 100%. Under the Fair and Equitable Test, the plan distributes as Realisable Value to dissenting secured senior creditors in a manner that they (1) retain the liens securing such claims and (2) receive deferred cash payments totalling the value of their claim. However, if the value of the collateral used to secure the claim is less than 110 in value, then the SME Debtor is only liable to pay that lower value to the secured creditor.

ii. Dissenting Senior Unsecured Creditors

Under the Relative Priority Test, the plan distributes as Realizable Value to dissenting unsecured senior creditor class any value lesser than 90.9% of their total claim price of 50. However, under the Fair and Equitable Test, the plan distributes any value between 10 to 50 as Realisable Value to this class.

iii. Dissenting Junior Unsecured Creditors

Under the Relative Priority Test, the plan distributes as Realisable Value to dissenting unsecured junior creditors class any value lesser than 80% of their total claim price of 30. Under the Fair and Equitable Test, the plan is distributed as Realisable Value to dissenting unsecured junior class any value between 0 to 60.

iv. Equity Holders

Under the Relative Priority Test, the value provided to the equity holders would be not more than 50% of its total value of 25. However, if the value provided to Class 2 and Class 3 is reduced, more value may be provided to the equity holders under Class 4. Under the Relative Priority Test, the equity holders cannot be provided with any value equal to or more than the percentage distributed to dissenting unsecured junior creditor class.

However, under the Fair and Equitable Test, it may be possible to even retain 100% of the total pre-petition equity. At the same time, this may be problematic in certain situations since in this scenario, the junior ranking classes are getting paid in full but not the higher classes. It may give rise to a heightened risk of opportunistic behaviour by the SME Debtors who may take advantage of the value at the cost of creditors, by forcing upon the creditors an involuntary curtailment and reduction of their claims.[104] This may further demote the already lower-ranked junior creditor classes including SME Creditors.[105]

Based on this understanding the following key differences between the Fair and Equitable Test and the Relative Priority Test are outlined:

- The Fair and Equitable Test provides more flexibility in comparison to the Relative Priority Test in permitting the SME Debtors to decide the distribution possibilities under the repayment plan. These distribution possibilities could be based on the pressing needs of the business and may increase the possibility of a successful restructuring of the SME Debtor. For instance, in certain situations, SME Debtors may find that providing a higher distribution (in percentage) to junior dissenting unsecured creditors than to the senior dissenting unsecured creditors, would increase the possibility of being able to revive its business.

- The equity holders retain a higher proportion of their equity interests in the Fair and Equitable Test than under the Relative Priority Test since the equity holders can only be provided a distribution (in percentage) which is lesser than the distribution (in percentage) provided to the most junior ranking creditor class, (unless a Relaxed Relative Priority Test approach is permitted). Under the Fair and Equitable Test, equity holders may be able to retain 100% of the pre-petition equity. However, this will not necessarily be the case in every scenario. In certain situations, equity holders may have to part with their equity interests if Best Interest of Creditors Test is not satisfied while making repayments under the restructuring plan to the dissenting creditors.

I will apply the conclusions based on this analysis in the next sub-section to compare the Fair and Equitable Test and the Relative Priority Test based on equity retention indicators.

5.2 Equity Retention Indicators

Based on the Working Definition of SME Debtors, an SME Debtor can be characterised as follows: (i) limited resources and lack of access to finance,[106] (ii) suffering from creditor passivity,[107] (iii) lack of incentives to access restructuring at an early stage of the formal insolvency process[108] and lastly (iv) from a macro-economic perspective, the failure of business might also lead to failures in the supply chain since its customers are also SMEs.[109] It can be identified that the SME Debtors face challenges associated with equity retention during their restructuring due to:

- Lack of incentives for early access to restructuring due to limited resources, lack of access to finance and creditor passivity

- From a macro-economic perspective, a well-functioning restructuring framework, equipped to handle a large number of cases in which the SME Debtors are able to participate is required. This restructuring framework, while balancing the creditor and debtor’s interests, should also provide an impetus to reduce the overall expenses and time required for restructuring an SME Debtor.

Based on this understanding, and expounding on the analysis conducted so far in this paper, I comparatively analyse equity retention abilities of the Relative Priority Test and the Fair and Equitable Test based on 3 indicators, (i) early access incentivisation, (ii) balancing of the creditor and equity holders’ interests and (iii) impetus for equity retention on a macro-economic scale.

5.2.1 Incentivising Early Access

The first equity retention indicator is the ability of the Relative Priority Test and Fair and Equitable Test to incentivise SME Debtors to access restructuring, at an early stage. Early access to restructuring would enable the SME Debtors to benefit from the timely use of restructuring proceedings and the option of drawing on specific knowledge, expertise and goodwill of the equity holder, which should incentivise approval of the plan.[110] Under the Fair and Equitable Test, unlike the Relative Priority Test, the leverage of reviving the business back on track would be the responsibility of the SME Debtor itself.[111] The Fair and Equitable Test shifts the burden upon equity holders to ensure that payments are made and business is revived. It increases the possibility of early access by equity holders to ensure that their reorganisation plan is successful since only the debtor can propose the plan under the Small Business Reorganization Act of 2019.[112] Additionally, as seen in Table A (Comparison of Distributional Possibilities under the Relative Priority Test and the Fair and Equitable Test), under the Fair and Equitable Test there is a higher possibility for equity holders to retain a higher proportion of their equity interests. The SME Debtors also have more flexibility to structure the distribution possibilities under the restructuring plan under the Fair and Equitable Test.[113]

The Fair and Equitable Test seems to provide more flexibility than the Relative Priority Test for consensual plan confirmation. Under the Fair and Equitable Test, the SME Debtor may retain equity interests even without provisioning for a relatively better treatment to the creditors (assuming that the Relaxed Relative Priority Test Approach is not applicable). Even if all classes reject a restructuring plan, it can still be crammed down on creditors if the plan does not discriminate unfairly and the Fair and Equitable Test is satisfied.[114] So long as the creditors have been promised returns based on the Projected Disposable Income, SME Debtors do not have to sacrifice their equity interests to pay for the claim amount for the creditors at the time of commencement of the reorganisation.[115]

All these factors evidence that the Fair and Equitable Test provides more incentives to the SME to access the restructuring at an early stage. Resultantly, based on this indicator, the Fair and Equitable Test seems to be relatively more effective in enabling the retention of equity interests for SME Debtors.

5.2.2 Balancing creditors’ and equity holders’ interests

The second equity retention indicator is based on the principle that a successful restructuring cannot be achieved by exploiting creditors or promoting the risk-taking behaviour of SME Debtors. Ultimately a balance has to be struck between creditor protection and debtor relief.[116] To understand this equity retention indicator I discuss two factors which balance these rights (i) preventing creditors’ exploitation and averting SME Debtor’s risk-taking behaviour and (ii) conferring protections for the rights of the creditors.

Scholars have argued that the Relative Priority Test may lead to the exploitation of creditors since an over-levered debtor may exploit the creditors by calculating the exact percentage of the claim amount required to satisfy the Relative Priority Test, and discharge the rest of the creditors.[117] This exploitation of creditors and risk-taking behaviour by SME Debtors is also possible under the Fair and Equitable Test. Although there are precedents mandating good faith while proposing the Projected Disposable Income under the Fair and Equitable Test, even under the Fair and Equitable Test, there remains a possibility that SME Debtors may project a low income to evade payments to creditors.[118] That being said, both the Small Business Reorganization Act of 2019 and Directive 2019/1023 acknowledge a situation where no prospect of survival exists for a business and state that such businesses should be liquidated, instead of restructuring.[119]

It has been suggested that Projected Disposable Income is successful in at least increasing the chances of achieving consensus in cases of disagreements between creditors and equity holders.[120] It promotes compromise since the creditors have lesser grounds to challenge the plan[121] and debtors would be mandated to satisfy Projected Disposable Income, which might curtail their discretion in the manner the SME Debtor’s income is used. Even if all classes reject a restructuring plan, it can still be crammed down on creditors if the plan does not discriminate unfairly and the Fair and Equitable Test is satisfied.[122] Based on the quantitative analysis under the Table, it may be concluded that it also increases the possibility of providing higher returns to the dissenting unsecured junior creditors lower in ranking, in comparison to the Relative Priority Test.[123] While the Directive 2019/1023 does provide Member States with the option to refuse to confirm a restructuring plan not having a reasonable prospect of preventing insolvency of the SME Debtor or ensuring the viability of the business,[124] it does not stipulate tests similar to the Reasonable Likelihood Test and the Default Remedies Test available for determination of the Projected Disposable Income under the Fair and Equitable Test. These tests assess whether the SME Debtor can realistically make payments under the repayment plan.[125] Additionally, the Directive 2019/1023 does not stipulate remedies such as liquidation of the assets of the SME Debtor for the protection of the creditors. This may reduce creditor exploitation by SME Debtors and curtail the risk-taking behaviour of SME Debtors and shift the burden on SME Debtors to make sure that the restructuring plan is successful.

Considering both these factors, it may be concluded that both the Relative Priority Test and the Fair and Equitable Test prevent creditor exploitation and avert risk-taking behaviour which may be taken by SME Debtors. However, the Fair and Equitable Test seems to relatively achieve a better balance between creditor rights protection and equity interests, in comparison to the Relative Priority Test, while enabling equity retention for SME Debtors during restructuring. Achieving this balance is also fruitful in achieving a consensual plan, as discussed in the next subsection.

5.2.3 Macro-economic perspective

SME Debtors’ equity interests’ retention enabling ability under the Relative Priority Test and the Fair and Equitable Test must be considered from a macro-economic perspective, considering that SME Debtors dominate the business needs in both EU and US.[126] To incentivise early access, a Fairness Test should, while balancing creditor and debtor’s interests, provide an impetus to reduce the overall expenses and time required for restructuring of an SME Debtor.[127] Therefore, equity retention based on the three indicators discussed above (i) Incentivising early access and (ii) balancing creditors’ and equity holders’ rights, would also result in furthering equity retention enabling the ability for SME Debtors on a macro-economic level.

With respect to the Relative Priority Test, scholars have contended that from a macroeconomic perspective since the Relative Priority Test depresses creditor recoveries, debt investments may decrease in EU, thereby negatively impacting the SME Debtors.[128] However, I believe that this argument is premised on the assumption that the introduction of the Relative Priority Test will necessarily decrease investor confidence in the preventive restructuring procedure which may not necessarily be true. Certain Member States are yet to implement the Directive 2019/1023 and so far, only Austria has implemented the Relative Priority Test under its Restructuring Code based on Directive 2019/1023.[129] Relative Priority Test’s application under the Austrian Restructuring Code has received support from scholars, who have symbolised this inclusion as ‘remarkable’.[130] The amended Austrian Restructuring Code only entered into force on 17 July 2021 and based on governmental statistics for the first quarter of 2022, insolvencies have more than doubled in the previous year in Austria.[131] However, these figures of course cannot be considered in isolation from other factors, including investor confidence in the new Austrian Restructuring Code in general and the effects of the COVID-19 pandemic.

On the other hand, the Small Business Reorganization Act of 2019, was enacted in the year 2020. The available statistics have so far indicated that the Fair and Equitable Test under the Small Business Reorganization Act of 2019, has been fruitful in bringing the intended reforms for SME Debtors to a certain extent. Existing data analysis, suggests that small businesses have been incentivised to file the Small Business Reorganization Act of 2019, proceedings. [132] The filings under the Small Business Reorganization Act of 2019, have increased by 21% in May 2022 compared to May 2021, although total bankruptcy filings have declined by 10%.[133] The US Trustee Program analysed a sub-set of 625 cases that were filed under the Small Business Reorganization Act of 2019, through June 30, 2020, and provided the following percentages as of September 2020:

- The percentage of confirmed plans under the Small Business Reorganization Act of 2019, was six times higher than the percentage of confirmed plans under the Small Business Cases.

- More than 60% of the confirmed plans were consensual.[134]

However, many important figures, based on which Fair and Equitable Test’s success may be evaluated would only be available in the year 2023, after the end of a 3-year period from the starting date of insolvency. For instance, the percentage of reorganised subchapter V SME Debtors that successfully satisfy their plan obligations than seeking further insolvency relief would be quite helpful but such information is not available.[135]

Therefore, it seems too early to assess based on statistical information and only time will tell, how successful the Relative Priority Test and Fair and Equitable Test in providing impetus to the overall restructuring process to incentivise equity retention by SME Debtors. SME Debtors have, however, shown confidence in both the Fair and Equitable Test and the Relative Priority Test, so far.

6. Concluding Remarks and Suggestions For EU Member States

Relative Priority Test under Article 11(1)(c) Directive 2019/1023, provides flexibility to the SME Debtors to retain while only providing relatively better treatment to more senior creditors, to enable equity retention. The Small Business Reorganization Act of 2019, on the other hand, provides for Projected Disposable Income based on the Fair and Equitable Test. The Small Business Reorganization Act of 2019, provides separate requirements for dissenting secured and unsecured creditors in a cram-down situation. This could not have been possible under the Directive 2019/1023 since Member States have their own procedural laws on insolvency and they differ vastly, on the manner in which the order of priorities for payment is regulated.

A quantitative analysis using a hypothetical case to compare the distributional possibilities under the Fair and Equitable Test and the Relative Priority Test reveals that there is a higher possibility of equity interests’ retention (in percentage) under the Fair and Equitable Test, in comparison to the Relative Priority Test. This is possible because, under the Relative Priority Test, equity interest holders cannot be provided with a relatively higher distribution (in percentage) than the distribution (in percentage) provided to the junior most ranking creditor class, while no such requirement exists under the Fair and Equitable Test. It may be possible under the Fair and Equitable Test for equity holders to even retain 100% of their equity interests in certain situations.

The Fair and Equitable Test provides more flexibility by permitting an SME Debtor to plan out the distribution possibilities under the repayment plan, based on the pressing needs and concerns of their business. This may increase the possibility of a successful restructuring of the SME Debtor, while it makes payments based on the repayment plan, in comparison to the Relative Priority Test under the Directive 2019/1023.

The comparative analysis of the Relative Priority Test with the Fair and Equitable Test based on four equity retention indicators shows that:

- SME Debtors may be relatively more incentivised to access the restructuring process at an early stage, under the Fair and Equitable Test in comparison to the Relative Priority Test, which increases the possibility of equity interests’ retention by SME Debtors under the Fair and Equitable Test.

- While both the Relative Priority Test and Fair and Equitable Test prevent creditor exploitation and avert risk-taking behaviour which SME Debtors may indulge in, Fair and Equitable Test seems to relatively achieve a better balance between creditors’ rights protection and equity interests.

- From a macro-economic perspective, it seems too early to assess based on available statistical information, the success of these Fairness Tests in enabling equity interests’ retention.

Based on these 3 indicators, it seems that the Fair and Equitable Test increases the possibility of enabling equity retention for SME Debtors during their restructuring, in comparison to the Relative Priority Test.

Premised on this analysis, I suggest that Member States may incorporate the Relative Priority Test as a Fairness Test in a manner that it enables retention of equity retention for SME Debtors. Member States may do so by finding orientation under the Fair and Equitable Test in the Small Business Reorganization Act of 2019. To allow the SME Debtors to gain from the equity interests’ retention enabling ability of the Fair and Equitable Test while implementing the Relative Priority Test, a Relaxed Relative Priority Test approach may be permitted. This Relaxed Relative Priority Test approach can be applied using the existing provisions under the Directive 2019/1023. Member States may permit SME Debtors under this Relaxed Relative Priority Test approach to either have a straight discharge procedure or alternatively make payments based on repayment plans, or a combination of both, by relying on Recital 45 of the Directive 2019/1023. If an SME Debtor chooses to make payments based on the repayment plan, Member States may provide for the following stipulations, by relying on Article 8(1)(h) and Article 10(3) Directive 2019/1023:

- A test similar to the Reasonable Likelihood Test to ensure that the SME Debtors will be able to make all the payments in a timely manner under the repayment plan, and

- Stipulation that SME Debtor is required to include protections within the plans, including liquidation of non-exempt assets and the satisfaction of a test similar to the Default Remedies Test to ensure that the rights of creditors are protected if payments under the repayment plan are not made.

Derogation from the Relative Priority Test under this Relaxed Relative Priority Test approach by relying on Article 11(2) of the Directive 2019/1023, may be permitted in two situations. Firstly, when equity retention is necessary for enabling a successful restructuring of the SME Debtor. Secondly, when the unsecured junior creditor classes would necessarily have to be provided better treatment (higher distribution in percentage) than the senior-ranking unsecured creditor classes. Such treatment may have to be provided to the unsecured junior creditor classes for the successful restructuring of the SME Debtor and for the SME Debtor to be reasonably able to make all the payments based on the repayment plan.

Mokal and Tirado, in my opinion aptly express how Member States should implement the Relative Priority Test:

‘The key now is for member states to particularise and implement the Relative Priority Test in a way that would facilitate fair and efficient restructurings … Restructuring law is ready for a dose of relativity.’[136]

In doing so, Member States may facilitate the retention of equity interests for restructuring of SME Debtors, by finding orientation in the Fair and Equitable Test under the Small Business Reorganization Act of 2019. It is hoped that the Member States will find some guidance pursuant to the suggestions stipulated above, to implement the Relative Priority Test in a manner that it strengthens the equity interests’ retention ability of the Relative Priority Test. It, however, remains to be seen whether for enabling equity interests’ retention for SME Debtors the Relative Priority Test may ‘herald restructuring law’s Einsteinian revolution’.[137]

[1] The author is grateful to Gert-Jan Boon, for his comments and inputs on a prior draft of this paper. This paper is based on the thesis submitted by the author for his Advanced Masters (ICCL) course at Leiden University. The author has also benefitted from the comments and inputs received from the reviewers at Herstructurering & Recovery Online (HERO).

[2] Office of Advocacy SBA, ‘Small Businesses Generate 44 Percent of the U.S. Economic Activity’, Release No. 19-1 ADV, January 30, 2019, available at <https://advocacy.sba.gov/2019/01/30/small-businesses-generate-44-percent-of-u-s-economic-activity/> (Accessed 11 January 2023); Recital 17, Directive 2019/1023.

[3] Gerhard Huemer, ‘The economic impact of COVID-19 on SMEs in Europe’, SME United, Crafts & SMEs in Europe, 30 June 2020, available at <https://www.smeunited.eu/admin/storage/smeunited/200630-covidsurvey-results.pdf> (Accessed 11 January 2023); Daniel Wilmoth, ‘The Effects of the COVID-19 Pandemic on Small Businesses’, Office of Advocacy, U.S. Small Business Administration, Issue Brief Number 16, March 2021, available at <https://cdn.advocacy.sba.gov/wp-content/uploads/2021/03/02112318/COVID-19-Impact-On-Small-Business.pdf> (Accessed 11 January 2023).

[4] Recital 2 and 3, Directive 2019/1023; In re Wildwoood Villages, LLC, (Bankr. M.D. Fla. May. 4, 2021), para. 6.

[5] Lorenzo Stanghellini et. Al, Best Practices in European Restructuring, Contractualised Distress Resolution in the Shadow of the Law, (2018, Wolters Kluwer), (‘CODIRE’), p. 34 at para 2.2.2; UNCITRAL Legislative Guide on Insolvency Law Part five: Insolvency law for micro and small enterprises, United Nations, Vienna 2022, available at <https://uncitral.un.org/sites/uncitral.un.org/files/media-documents/uncitral/en/msms_insolvency_ebook.pdf> (Accessed 11 January 2023) (‘UNCITRAL MSME Guide’) p. 41; European Law Institute (ELI), ‘Rescue of Business in Insolvency Law’, 2017 available at <https://www.europeanlawinstitute.eu/fileadmin/user_upload/p_eli/Publications/Instrument_INSOLVENCY.pdf> (Accessed 11 January 2023) (‘ELI Business Rescue Report’), p. 367-374.

[6] Recital 3, Directive 2019/1023; In re Wildwood Villages, LLC, (Bankr. M.D. Fla. May. 4, 2021), para. 6.

[7] CODIRE, above note 5, p. 32.

[8] As per Article 1(2), Directive 2019/1023, affected parties means creditors, including, where applicable under national law, workers, or classes of creditors and, where applicable, under national law, equity holders, whose claims or interests, respectively, are directly affected by a restructuring plan.

[9] Article 9 of the Directive 2019/1023 provides the conditions for the adoption of a restructuring plan; SBRA provides rules for confirmation of a plan under 11 USC § 1129 and 11 USC § 1191(c).

[10] Article 11 Directive 2019/1023; 11 USC § 1129(b)(1).

[11] Article 11(2) Directive 2019/1023.

[12] Article 11(1)(c) Directive 2019/1023.

[13] Inclusion was made by the Proposal for a directive of the European Parliament and of the Council on preventive restructuring frameworks, second chance and measures to increase the efficiency of restructuring, insolvency and discharge procedures and amending Directive 2012/30, Brussels 17 December 2018, 15556/18, 2016/0359(COD), Article 11(1)(c) at p. 73 available at <https://data.consilium.europa.eu/doc/document/ST-15556-2018-INIT/en/pdf> (Accessed 11 January 2023).

[14] R.J. de Wijs et al, ‘The Imminent Distortion of European Insolvency Law: How the European Union Erodes the Basic Fabric of Private Law by allowing ‘Relative Priority (RPR)’ (2019) University of Amsterdam, UvA-Dare (Digital Academy Repository), 125(4), p. 477-493 (‘De Weijs et. Al. Imminent Distortion of Insolvency Law’); Bob Wessels, ‘2019-03-doc10 The full version of my reply to professor De Weijs et al’, 22 March 2019, available at <https://bobwessels.nl/blog/2019-03-doc10-the-full-version-of-my-reply-to-professor-de-weijs-et-al/> (Accessed 11 January 2023) (‘Bob Wessels Reply’); Stephan Madaus, ‘Leaving the Shadows of US Bankruptcy Law: A proposal to divide the realms of Insolvency and Restructuring Laws’, 4 June 2018, Eur Bus Org Law Rev (2018) 19:615–647 available at <https://doi.org/10.1007/s40804-018-0113-7> (Accessed 11 January 2023) (‘Madaus Leaving shadows of US Bankruptcy Law’); Riz Mokal and Ignacio Tirado, ‘Has Newton had his day? Relativity and realism in European Restructuring’, Butterworths Journal of International Banking and Financial Law, April 2019, (‘Mokal and Tirado’); Giulia Ballerini, ‘The Priorities dilemma in the EU preventive restructuring directive: Absolute or relative Priority Rule?’ (2020) Wiley, INSOL International available at <10.1002/iir.1399> (Accessed 11 January 2023) (‘Ballerini’); Jonathan M. Seymour and Steven L. Schwarz, ‘Corporate Restructuring under Relative and Absolute Priority Default Rules: A comparative assessment’, University of Illinois Law Review 2021 U. III. L. Rev. (‘Seymour and Schwarz’).

[15] R.J. De Weijs, ‘Preventive restructuring framework and the last-minute introduction of Relative Priority, (20 March 2019, Letter to the European Parliament Committee Juri (Legal Affairs) Rappoteurs) available at <https://drive.google.com/file/d/1l4Xeljvi2LjarI5aR6c7DBUv3YX2OlNa/view> (Accessed 11 January 2023), p. (‘De Weijs Letter’) p. 5; Douglas G. Baird, (March 7, 2019, Letter addressed to Prof. De Weijs) available at <https://drive.google.com/file/d/1l4Xeljvi2LjarI5aR6c7DBUv3YX2OlNa/view> (Accessed 11 January 2023), (‘Douglas Baird’s Letter’).

[16] The theorisation of the Relative Priority Rule in the US – such as the SME Equity Retention Plan and the New Value Exception seem – is quite different from its theorisation in the European context. Be that as it may, this does not prima facie impede its credibility or make it any less fair as a priority test, in so far as its equity retention enabling function is concerned. For a discussion on the same refer to Raghav Mittal, ‘Prioritizing SME Debtor’s Equity Retention: Espousing Relativity over Fairness and Equitability? Comparing Relative Priority Rule with Fair and Equitable Test’, Thesis, Leiden University, available at

<https://www.burenlegal.com/sites/default/files/usercontent/contentfiles/Raghav%20Mittal_%20Thesis%20version%2012%20July%202022__0.pdf > (Accessed 11 January 2023), (‘Raghav Mittal Thesis’) para. 4.2.

[17] 11 USC § 1191(c).

[18] CODIRE above note 5, p.34.

[19] UNCITRAL MSME Guide above note 5, p. 41-42.

[20] CODIRE above note 5, p. 34.

[21] CODIRE above note 5, p. 17.

[22] See for instance the criteria used for defining SMEs under Article 2(c) and Recital 18 Directive 2019/1023; Directive 2013/14 of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings amending directive 2006/43/EC of the European Parliament and repealing council directives 78/660/EEC and 83/349/EEC; Under the Small Business Reorganization Act of 2019, the criteria for defining SMEs has been provided under 11 USC § 1182(1).

[23] Article 2(c) Directive 2019/1023.

[24] Madaus Stephan, European Parliament, Legal and Parliamentary Affairs, ‘The Impact of SMEs of the Proposal of Preventive Restructuring, Second Chance and Improvement Measures, In-depth Analysis of the JURI Committee, May 2017, Directorate General for Internal Policies of the Union, Policy Department for Citizens’ Right and Constitutional Affairs, p. 7.

[25] 11 USC § 101(51D) and 11 USC § 1182 (1).

[26] European Law Institute (ELI), ‘Rescue of Business in Insolvency Law’, 2017 available at <https://www.europeanlawinstitute.eu/fileadmin/user_upload/p_eli/Publications/Instrument_INSOLVENCY.pdf> (Accessed 11 January 2023) (‘ELI Business Rescue Report’)

[27] UNCITRAL MSME Guide, above note 5, p. 42 at para. 12.

[28] ELI Business Rescue Report, above note 5, para. 749; CODIRE, above note 5, p. 34 at para. 2.2.2.

[29] World Bank Group Insolvency and Creditor/Debtor Regimes Task Force, Working Group on the Treatment of MSME Insolvency, ‘Report on the Treatment of MSME Insolvency’, 2017, International Bank for Reconstruction and Development/the World Bank (‘World Bank Report’), p. 12.

[30] ELI Business Rescue Report, above note 5, para. 756.

[31] ELI Business Rescue Report, above note 5, para. 371.

[32] Recital 2 and 3 Directive 2019/1023; In re Wildwoood Villages, LLC, Bankr. M.D. Fla. May. 4, 2021, p. 6.

[33] As per Article 1(2) of the Directive 2019/1023 affected parties means creditors, including, where applicable under national law, workers, or classes of creditors and, where applicable, under national law, equity holders, whose claims or interests, respectively, are directly affected by a restructuring plan.

[34] Article 9 Directive 2019/1023 provides the conditions for the adoption of a restructuring plan; Article 10 Directive 2019/1023 provides certain situations where the Member States shall ensure the restructuring plans are confirmed by a judicial or administrative authority if they are to be binding upon the parties; The Small Business Reorganization Act of 2019, provides rules for confirmation of a plan under 11 USC, §§ 1129 and 1191(c).

[35] CODIRE above note 5, p. 32.

[36] CODIRE above note 5, p. 33.

[37] Ibid.

[38] Bob Wessels Reply, above note 14.

[39] Ibid.

[40] CODIRE above note 5, p. 33-34; Bob Wessels Reply, above note 14.

[41] Article 10(2)(d) Directive 2019/1023.

[42] Recital 50, 52 and Article 1(6) Directive 2019/1023; 11 USC § 1129(a)(7).

[43] Art. 1(6) Directive 2019/1023.

[44] Mokal and Tirado, above note 14, p. 233.

[45] Stephan Madaus, ‘Is the Relative Priority Rule right for your jurisdiction? A simple guide to RPR’, 18 January 2020, WP 2020-1 (‘Simple Guide to RPR’) p. 2-3.

[46] Ibid, p. 1-2.

[47] Article 10(1)(a) Directive 2019/1023.

[48] Article 11(1) Directive 2019/1023.

[49] Article 10(3) Directive 2019/1023.

[50] Recital 54 and Article 11(1)(b) Directive 2019/1023.

[51] Article 11(1)(d) Directive 2019/1023.

[52] The Directive 2019/1023 gives the Member states a choice between enacting Absolute Priority Test or RPR.

[53] Article 11(1)(c) Directive 2019/1023.

[54] De Weijs et. al. Imminent Distortion of European Insolvency Law above note 14, p. 17-19.

[55] In De Weijs et. al. Imminent Distortion of European Insolvency Law above note 14, p. 18, this has been suggested as one of the possible standards amongst others.

[56] Simple Guide to RPR, above note 45, Example 9, p. 6.

[57] As phrased in the Simple Guide to RPR above note 45, p. 4.

[58] Article 11(2) Second paragraph Directive 2019/1023.

[59] Simple Guide to RPR, above note 45, p. 6.

[60] Recital 45 Directive 2019/1023.

[61] Mokal and Tirado, above note 14, p. 235.

[62] Simple Guide to RPR, above note 45, p. 6.

[63] CODIRE, above note 5, p. 5.

[64] Ibid.

[65] CODIRE above note 5, p. 46-47. These strategies are commonly referred to as ‘loan-to-own’ strategies.

[66] De Weijs et. Al. Imminent Distortion of Insolvency Law, above note 14, p. 2.

[67] De Weijs Letter, above note 15, 4-5.

[68] Congress House of Representatives, 'Small Business Reorganisation Act, 2019’, Judiciary Committee Report 116-171, 116th Congress 1st Session, available at < https://www.govinfo.gov/content/pkg/CRPT-116hrpt171/pdf/CRPT-116hrpt171.pdf> (Accessed 11 January 2023) (‘Judiciary Committee Report’), p. 1.

[69] 11 USC § 1189(a).

[70] 11 USC § 1129(a)(8).

[71] 11 USC § 1191(b).

[72] 11 USC § 1191(b).

[73]11 USC § 1129(a)(7)(A)(ii).

[74] 11 USC § 1191(c).

[75] 11 USC § 1129(b)(2)(A)(i).

[76] 11 USC §§ 1129(b)(2)(A)(ii) and 1191(c)(1).

[77] 11 USC § 1129(2)(B)(2)(ii); In re Murel Holding Corp, 75 F 2d 941 (2nd Circuit, 1935); Legislative statements, Historical and Revision Notes, 11 USC § 1129, available at

<https://uscode.house.gov/view.xhtml?path=/prelim@title11/chapter11&edition=prelim> (Accessed 11 January 2023).

[78]11 USC § 1191(c)(2).

[79] 11USC § 1191(c)(2)(A).

[80] 11 USC § 1191(c)(2)(B).

[81] 11 USC § 1191(d).

[82] 11 USC § 1191(d).

[83] Paul W. Bonapfel, ‘A Guide to the Small Business Reorganisation Act of 2019’, (Revised May 2022), Originally published at 93 Amer. Bankr. L.J. 571 (2019), p. 134.

[84] In Legal Services Bureau v. Orange County Bail Bonds Inc., Cal. Ct. App. Apr. 5, 2021, p. 12-13.

[85] In re Urgent Care Physicians, Ltd., Bankr. E.D. Wis. Dec. 20, 2021, p. 17-18.

[86] 11 USC § 1191(c)(3)(A)(i).

[87] 11 USC § 1191(c)(3)(A)(ii).

[88] In re Pearl Resources LLC, 622, B.R. 236, Bankr. S.D. Tex. 2020, para. 268.

[89] 11 USC § 1191(c)(3).

[90] In re Urgent Care Physicians, Ltd., Bankr. E.D. Wisc. 2021, para. 19-20.

[91] Brian Shaw, ‘2 years of Small Biz Bankruptcy Law: Winners and Losers’ (April 4, 2022) available at <https://www.law360.com/articles/1480550/2-years-of-small-biz-bankruptcy-law-winners-and-losers> (Accessed 11 January 2023) (‘Brian Shaw’).

[92] 11 USC Section 1191 (b).

[93] 11 USC Section 1181(c); Christopher G. Bradley, ‘The New Small Business Bankruptcy Game: Strategies for Creditors under the Small Business Reorganization Act’ 2020, Law Faculty Scholarly Articles, 649, available at <https://uknowledge.uky.edu/cgi/viewcontent.cgi?article=1648&context=law_facpub> (Accessed 11 January 2023) (‘Bradley’).

[94] 11 USC § 1191(c)(3)(A) and 11 USC § 1191(c)(3)(B).

[95] Ballerini, above note 14, p. 22.

[96] In re Thomas Young, Opinion No. 20-11844-t11, available at <https://www.govinfo.gov/content/pkg/USCOURTS-nmb-1_20-bk-11844/pdf/USCOURTS-nmb-1_20-bk-11844-0.pdf> (Accessed 11 January 2023), para. 11-12.

[97] Bradley, above note 93, p. 256-257.

[98] European Commission, Directorate-General for Justice and Consumers, Dahlgreen, J., Brown, S., Keay, A., et al., ‘Study on a new approach to business failure and insolvency: comparative legal analysis of the Member States relevant provisions and practices’, Publications Office, 2016, available at <https://data.europa.eu/doi/10.2838/87512> (Accessed 11 January 2023), p. 112.

[99] Ibid, p. 114.

[100]11 USC § 1191(c).

[101] 11 USC § 1191(c).

[102] Simple Guide to RPR above note 45, Example 7 on p. 5.

[103] Recital 78 and Article 21(1) Directive 2019/1023; In re Urgent Care Physicians Ltd., Bankr. E.D. Wis. Dec. 20, 2021, para. 18.

[104] Dr. R.J. de Weijs, A.L. Jonkers and M. Malakotipour LLB, ‘A reply to professor Madaus “The new European Relative Priority from the Preventive Restructuring Directive – The end of European Insolvency Law?”, Corporate Finance Lab, March 15, 2019, available at <https://corporatefinancelab.org/2019/03/15/a-reply-to-professor-madaus-the-new-european-relative-priority-from-the-preventive-restructuring-directive-the-end-of-european-insolvency-law/> (Accessed 11 January 2023)

[105] Jonathan McCarthy, ‘A Class Apart: The Relevance of the EU Preventive Restructuring Directive for Small and Medium Enterprises’, European Business Organisation Law Review (2020) 21:895-913, p. 903-904

[106] Peer Stein, Oya P. Pinar Ardic, and Martin Hommes, ‘Closing the Credit Gap for Formal and Informal Micro, Small, and Medium Enterprises’, (2013, Washington), available at <https://openknowledge.worldbank.org/handle/10986/21728> (Accessed 11 January 2023), p. 11; ELI Business Report, above note 5, para. 754-755.

[107] World Bank Report above note 29, p. 12; ELI Business Rescue Report above note 5, para. 756.

[108] CODIRE above note 5, p. 234 at para 1.2.

[109] ELI Business Rescue Report above note 5, para. 757-758.

[110] CODIRE above note 5, p. 46 and 47.

[111] NetJets Aviation, Inc. v. RS Air, LLC, WL 1288608, B.A.P. 9th Cir. 2022, 8-9; National Loan Invs. v. Rickerson (In re Rickerson), 636 B.R., Bankr. W.D. Pa. 2021, para. 416-422.

[112] 11 USC § 1189 (a).

[113] Discussed under section 5.1 of this Paper.

[114] 11 USC § 1191.

[115] 11 USC § 1191(c).

[116] Recital 3 Directive 2019/1023; In re Wildwoood Villages, LLC, Bankr. M.D. Fla. May. 4, 2021, para. 6.

[117] De Weijs, Imminent Distortion of EU Law above note 14, para. 6.2.

[118] In re, Thomas Young and Connie Young, Opinion No. 20-11844-t11, available at <https://www.govinfo.gov/content/pkg/USCOURTS-nmb-1_20-bk-11844/pdf/USCOURTS-nmb-1_20-bk-11844-0.pdf> (Accessed 11 January 2023), para. 7-8.

[119] Recital 3 and 24 Directive 2019/1023; In re, Thomas Young and Connie Young, Opinion No. 20-11844-t11, available at <https://www.govinfo.gov/content/pkg/USCOURTS-nmb-1_20-bk-11844/pdf/USCOURTS-nmb-1_20-bk-11844-0.pdf> (Accessed 11 January 2023), para. 7-8.

[120] Brian Shaw, above note 91.

[121] For reference see Raghav Mittal Thesis, above note 16, Section 3.3.

[122] 11 USC § 1191(b)

[123] Discussed under section 5.1 of this Paper.

[124] Article 8(1)(h) and Article 10(3) Directive 2019/1023.

[125] For reference see Raghav Mittal Thesis, above note 16, Section 3.3.

[126] Recital 17 Directive 2019/1023; Judiciary Committee Report, above note 68, p. 2; ELI Business Rescue Report above note 5, p. 367-368.

[127] ELI Business Rescue Report, above note 5, para. 371; Discussed under 5.2.1 of this Paper.

[128] Seymour and Schwarz above note 14, p. 40.

[129] Section 36 Restructuring Code, Austria, (Restrukturierungsordnung), CELEX No. 32109L1023 available at <https://www.ris.bka.gv.at/GeltendeFassung.wxe?Abfrage=Bundesnormen&Gesetzesnummer=20011622> (Accessed 11 January 2023); For details of the National Transposition measures by Member States refer to European Union, National transposition Measures communicated by Member States concerning Directive EU/ 2019/1023, Document No. 32019L1023 available at <https://eur-lex.europa.eu/legal-content/EN/NIM/?uri=celex:32019L1023> (Accessed 11 January 2023).

[130] Georg Wabl and Martin Trenker, ‘Special Issue Preventive Restructuring 5. The Austrian Implementation of the Directive 2019/1023: Game Changer or Missed Opportunity?’, HERO/W-005, 8 July 2022, available at <https://www.online-hero.nl/art/4358/special-issue-preventive-restructuring-5-the-austrian-implementation-of-the-prd-2019-game-changer-or-missed-opportunity> (Accessed 11 January 2023).

[131] Statistics Austria, ‘Bankruptcies sharply increased again in the first quarter of 2022; registrations decreased’, Press release: 12.808-106/22 available at

<https://www.statistik.at/fileadmin/announcement/2022/05/20220510InsolvenzenQ12022EN.pdf> (Accessed 11 January 2023); Also see press release 12.731-029/22, ‘Bankruptcies in the fourth quarter of 2021 above pre-crisis level; continued slowdown in registrations’ available at <https://www.statistik.at/fileadmin/announcement/2022/05/20220209Insolvenzen2021Q4EN.pdf> (Accessed 11 January 2023).

[132] Epiq Bankruptcy, ‘The Future of Subchapter V: Navigating the Pandemic and Beyond’ available at <https://bankruptcy.epiqglobal.com/blog/the-future-of-subchapter-v-navigating-the-pandemic-and-beyond-0> (Accessed 11 January 2023).

[133] Epiq Bankruptcy, ‘May Total Commercial Chapter 11 Bankruptcy Fillings Increased 34 percent over the same period last year’, 3 June 2022, available at <https://www.epiqglobal.com/en-us/resource-center/news/may-commercial-chapter-11-bankruptcies-increase> (Accessed 11 January 2023).

[134] Clifford J White, ‘Small Business Reorganisation Act: Implementation and Trends’, American Bankruptcy Institute Journal, Vol. XL, No.1 January 2021, available at <https://www.justice.gov/ust/page/file/1350736/download> (Accessed 11 January 2023).

[135] Brian Shaw, above note 91.

[136] Mokal and Tirado, above note 14, p. 235.

[137] Ibid.

Keywords

Auteur(s)

is an Indian-qualified lawyer and an Advanced Masters ICCL graduate from Leiden University.

is a Bank Insolvency Intern with the International Institute for Unification of Private Law (UNIDROIT), Rome.